In the landscape of personal finance, there are very few genuine “cheat codes.” We are taught to max out our 401(k) plans, fund our Roth IRAs, and open taxable brokerage accounts once the tax-advantaged buckets are full. Yet, the most powerful wealth-building tool in the entire United States tax code is routinely treated as nothing more than a glorified medical checking account.

That tool is the Health Savings Account (HSA).

According to long-term retirement data from major financial institutions like Fidelity Investments and Vanguard, the vast majority of HSA owners use their accounts strictly for short-term liquidity. They contribute cash, experience a medical expense, and immediately withdraw the funds to pay the bill. While this saves money on taxes in the short term, it completely misses the macroeconomic engine under the hood. To unlock the true, compounding power of this vehicle, you need to transition from an HSA spender to an HSA investor.

To achieve this, selecting the best HSA investment funds is paramount. By choosing low-cost, high-performing vehicles and letting your contributions compound over decades, you can build a tax-free healthcare nest egg capable of funding your retirement. This comprehensive guide breaks down the absolute best HSA investment funds available, analyzes the underlying mechanics of HSA growth, and offers actionable asset allocation frameworks to optimize your long-term returns.

What Is an HSA and Why It Is Unique

A Health Savings Account is a personal savings account designed specifically to help individuals save for qualified medical expenses. However, unlike a Flexible Spending Account (FSA), an HSA is not a “use-it-or-lose-it” vehicle. The money you contribute belongs to you permanently. It rolls over from year to year, accumulates interest, can be invested in the financial markets, and remains yours even if you change employers or retire.

To be eligible to open and contribute to an HSA, the Internal Revenue Service (IRS) requires that you be enrolled in an HSA-qualified High-Deductible Health Plan (HDHP). The IRS updates the specific parameters for these plans annually to account for inflation. You can read the formal guidelines and compliance criteria directly in IRS Publication 969.

For the 2026 calendar year, the official thresholds and contribution maximums are as follows:

| Parameter | Self-Only Coverage (2026) | Family Coverage (2026) |

| Minimum Annual Deductible | $1,700 | $3,400 |

| Maximum Out-of-Pocket Limit | $8,500 | $17,000 |

| Maximum Annual Contribution Limit | $4,400 | $8,750 |

| Catch-Up Contribution (Age 55+) | $1,000 | $1,000 |

Note on Employer Contributions: The annual contribution limits established by the IRS apply to the combined total of both your personal contributions and any seed money or matching funds provided by your employer. If your company contributes $1,000 to your family HSA in 2026, your personal contribution ceiling is capped at $7,750.

Understanding these structural mechanics matters because an HSA is explicitly structured to support long-term capital preservation and accumulation if paired with the right high-quality investment choices.

Why Investing HSA Funds Can Be Powerful for Long-Term Wealth Building

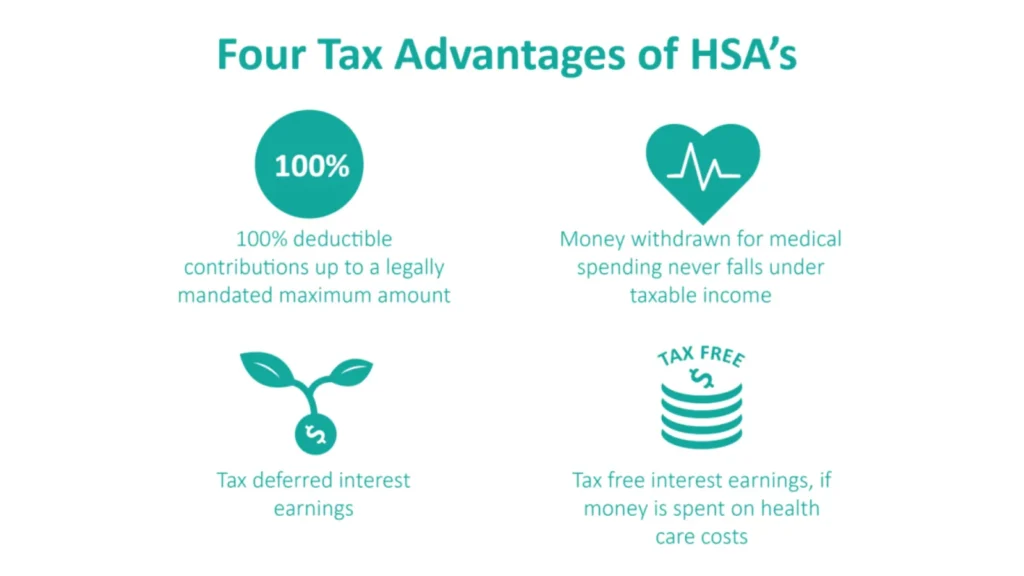

The core reason investing HSA funds is a revolutionary wealth-building strategy boils down to a singular phrase: the triple tax advantage. No other investment vehicle—not the traditional IRA, the Roth IRA, or the employer-sponsored 401(k)—provides three distinct layers of tax insulation simultaneously.

The Triple Tax Advantage Broken Down

- Tax-Deductible Contributions: Every dollar you contribute to an HSA reduces your adjusted gross income (AGI) for the year on a dollar-for-dollar basis. Better yet, if your contributions are processed via automated payroll deductions under an employer’s Section 125 cafeteria plan, those funds bypass Federal Insurance Contributions Act (FICA) taxes, instantly saving you an extra 7.65%.

- Tax-Free Growth: Once your cash is safely inside the account, any dividends, interest payments, or capital gains generated by your selected asset classes accumulate with zero tax drag. You do not owe annual taxes on capital gains distributions, allowing your money to compound faster.

- Tax-Free Withdrawals: When you withdraw funds to pay for qualified medical expenses—ranging from routine dental cleanings and prescription eyeglasses to major hospital procedures and long-term care insurance premiums—the distributions are 100% tax-free.

The Long-Term “Shoebox” Strategy

To appreciate why you should invest HSA funds for the long run, consider the stark contrast between standard retirement accounts and an HSA utilized via the “shoebox strategy.”

With a traditional 401(k), you avoid taxes today but pay standard income tax when you withdraw the money in retirement. With a Roth IRA, you pay taxes upfront, but the growth and retirement withdrawals are clean. An HSA combined with the best HSA investment funds beats both systems: it is tax-free on the way in, tax-free while it sits there, and tax-free on the way out.

[Traditional 401(k)] ---> Tax-Free Input ---> Taxable Output

[Roth IRA] ---> Taxable Input ---> Tax-Free Output

[Health Savings A/C] ---> Tax-Free Input ---> Tax-Free Output (For Medical)

The optimal strategy for those who can afford it is to pay for current out-of-pocket medical bills using regular cash flow (checking accounts or credit cards) while leaving the HSA fully invested in equities. The IRS does not impose a deadline or expiration date on when you must claim a reimbursement for a medical expense.

As long as the expense occurred after you initially established your HSA, you can save your digital receipts (“shoeboxing” them) for 15, 20, or 30 years. During that multi-decade span, your invested capital compounds exponentially. When you eventually decide to pull the money out during retirement, you can cash in those decades-old receipts to execute a massive, completely tax-free withdrawal for any purpose whatsoever.

Furthermore, once you reach age 65, the 20% non-qualified withdrawal penalty disappears entirely. If you happen to have excess funds in your HSA that aren’t tied to a medical receipt, you can withdraw them for non-medical reasons. At that stage, the account functions identically to a traditional IRA—you simply pay ordinary income tax on the distribution. If you use it for healthcare, it remains completely tax-free.

Key Factors to Consider Before Choosing HSA Investment Funds

Before diving directly into fund selections, you must evaluate the operational constraints and structural variables unique to HSA accounts. Not all HSA administrators are created equal, and not all investment choices fit every individual financial plan.

1. Liquidity Buffers and Cash Investment Thresholds

Many employer-chosen HSA providers, such as HealthEquity or HSA Bank, impose a mandatory cash threshold rule. They require you to maintain a minimum cash balance—frequently $1,000 or $2,000—in a low-yield savings tier before you are permitted to sweep any excess dollars into the investment portal.

When mapping out your asset allocation, remember to factor in this “cash drag.” If your provider requires a $2,000 cash floor and you have $4,400 in total account value, nearly 45% of your portfolio is stuck earning minimal interest. To counter this, your remaining investable dollars must work efficiently in low-cost equities. Platforms like Fidelity’s retail HSA are exceptions, offering $0 cash minimums and allowing you to invest from the very first dollar.

2. Expense Ratios and Invisible Administration Fees

When evaluating HSA investment funds, expense ratios represent the single most reliable predictor of future relative performance. An expense ratio is the annual fee charged by a mutual fund or Exchange-Traded Fund (ETF) expressed as a percentage of your total investment.

For instance, a fund with a 0.50% expense ratio costs you $50 annually for every $10,000 invested, whereas an institutional-grade index fund charging 0.02% costs just $2 per year. Over a 30-year accumulation horizon, that minor delta can compound into tens of thousands of dollars lost to asset managers. Seek out ultra-low-cost index funds or broad-market ETFs.

3. Account Custodian Constraints and Fund Menus

If your HSA is locked into an employer-sponsored platform, your investment menu may be curated down to a finite list of 15 to 30 mutual funds. In these situations, your goal is to locate the core building blocks: a broad U.S. large-cap index, a total international index, and a high-quality bond fund.

If your employer’s plan features exclusively high-fee, actively managed options, remember that you are legally entitled to execute a tax-free trustee-to-trustee transfer or a once-per-year rollover to an independent, self-directed HSA provider of your own choosing (such as Charles Schwab or Fidelity) to gain access to an open brokerage menu with thousands of options.

Best HSA Investment Funds (Detailed Analysis and Comparisons)

To build an institutional-grade portfolio within your HSA, you should lean heavily on broad-market, low-cost index products. Academic research continuously confirms that passive index tracking outperforms active management over long horizons after accounting for fees.

Below is a granular analysis of the absolute best HSA investment funds across the industry, categorized by asset class and provider availability.

1. Broad U.S. Equity & Large-Cap Index Funds

These funds serve as the foundational bedrock of any long-term growth portfolio. They track the largest, most resilient companies in the American economy, capturing broad corporate earnings growth.

- Fidelity 500 Index Fund (FXAIX): This is arguably the gold standard for large-cap investing. With an exceptionally low net expense ratio of 0.015%, it tracks the S&P 500 Index with near-perfect precision. It offers exposure to roughly 500 of the largest publicly traded U.S. companies, providing massive diversification through a single ticker.

- Vanguard 500 Index Fund Admiral Shares (VFIAX) / Vanguard S&P 500 ETF (VOO): If your HSA platform offers Vanguard products, VOO (ETF) or VFIAX (Mutual Fund) are ideal choices. Charging 0.03%, these funds are highly liquid, tracking the identical S&P 500 framework as Fidelity’s offering.

- Schwab S&P 500 Index Fund (SWPPX): Charles Schwab’s flagship index offering carries a rock-bottom expense ratio of 0.02% with no investment minimums, making it an excellent anchor asset for retail HSA accounts.

2. Total Stock Market Index Funds

For investors who want exposure not just to large-cap giants but also to mid-cap and small-cap companies that can accelerate portfolio growth during economic expansions, total market funds are the optimal route.

- Vanguard Total Stock Market ETF (VTI) / VITAX: Tracks the CRSP US Total Market Index, giving you exposure to over 3,700 stocks across the entire capitalization spectrum. Expense ratio: 0.03%.

- Fidelity Total Market Index Fund (FSKAX): Provides identical all-cap exposure to the entire investable domestic equity universe for a razor-thin expense ratio of 0.015%.

3. International & Total Global Equity Index Funds

Excluding companies outside the United States introduces geographic concentration risk. Adding international exposure ensures your HSA participates in global economic growth.

- Vanguard Total International Stock ETF (VXUS): Captures both developed and emerging markets outside the United States, including thousands of holdings across Europe, Asia, and Latin America. Expense ratio: 0.08%.

- Fidelity International Index Fund (FSPSX): Focuses predominantly on developed international markets (omitting emerging markets for a tighter risk profile) at a lean expense ratio of 0.035%.

4. Fixed Income & Broad Core Bond Index Funds

If you have a shorter timeline or prefer lower volatility to ensure money is readily accessible for near-term medical needs, high-quality bond index funds are essential.

- Fidelity U.S. Bond Index Fund (FXNAX): Tracks the Bloomberg US Aggregate Bond Index, offering broad exposure to investment-grade corporate bonds, U.S. Treasuries, and asset-backed securities. Expense ratio: 0.025%.

- Vanguard Total Bond Market ETF (BND): The premier choice for broad fixed-income exposure, providing steady income yield with low price volatility. Expense ratio: 0.03%.

Comprehensive Fund Comparison Table

To help you visually compare and contrast these top-tier options, the table below consolidates the vital metrics for the best HSA investment funds available today:

| Ticker | Fund Name | Asset Class | Expense Ratio | Primary Benefit |

| FXAIX | Fidelity 500 Index Fund | U.S. Large-Cap | 0.015% | Absolute lowest cost for S&P 500 exposure. |

| VOO | Vanguard S&P 500 ETF | U.S. Large-Cap | 0.03% | Extreme liquidity, institutional stability. |

| SWPPX | Schwab S&P 500 Index | U.S. Large-Cap | 0.02% | Zero minimum investment constraints. |

| VTI | Vanguard Total Stock Market | Total U.S. Equity | 0.03% | Captures small and mid-cap upside. |

| FSKAX | Fidelity Total Market Index | Total U.S. Equity | 0.015% | Comprehensive domestic market coverage. |

| VXUS | Vanguard Total International | Global Equity | 0.08% | Broadest cross-border diversification. |

| FSPSX | Fidelity International Index | Developed Markets | 0.035% | Low-cost exposure to mature global giants. |

| FXNAX | Fidelity U.S. Bond Index | Fixed Income | 0.025% | Ideal for capital preservation and yield. |

| BND | Vanguard Total Bond Market | Fixed Income | 0.03% | Highly defensive, stable core bond exposure. |

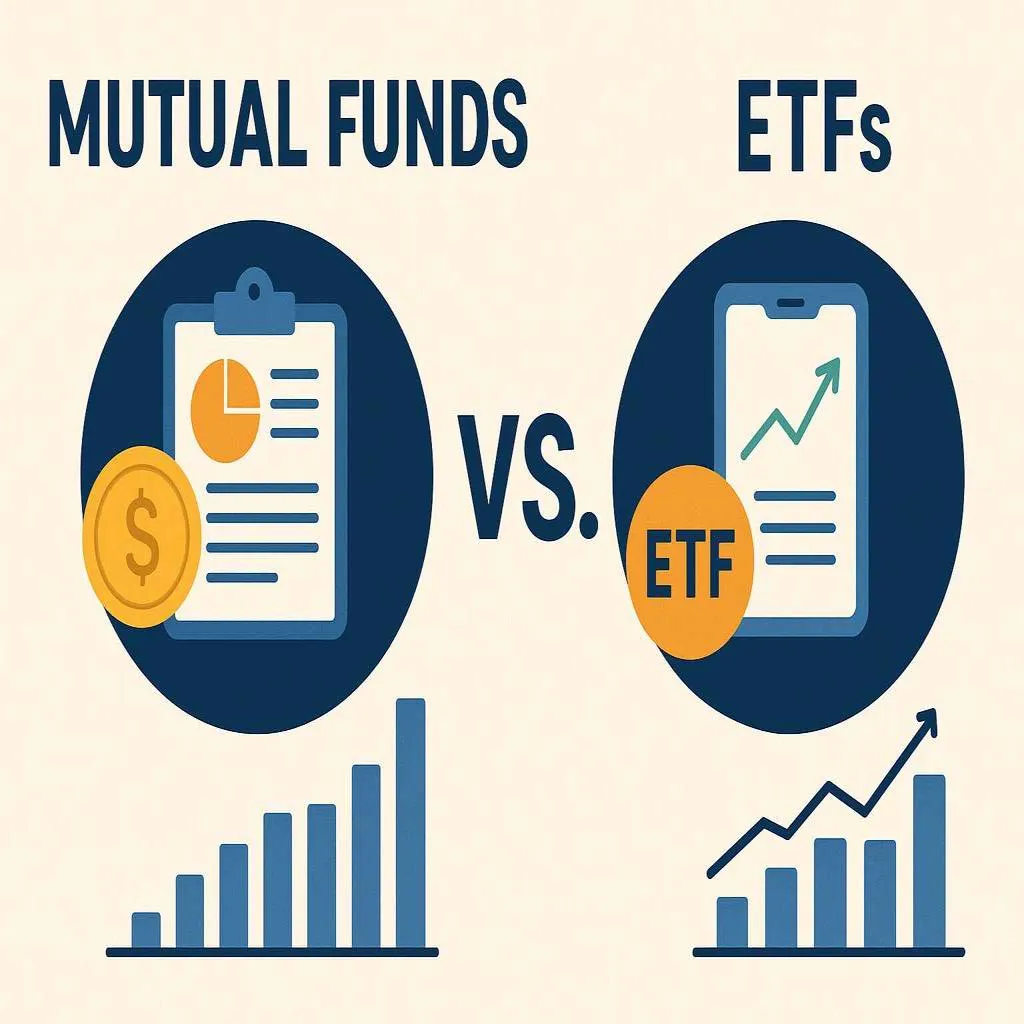

Index Funds vs ETFs vs Target-Date Funds for HSA Investors

When planning the best way to invest HSA funds, you will encounter three distinct vehicle structures: Index Mutual Funds, Exchange-Traded Funds (ETFs), and Target-Date Funds (TDFs). Choosing the right vehicle depends heavily on your automated cash inflow strategy.

Index Mutual Funds

Index mutual funds trade once per day after the market closes at the Net Asset Value (NAV). For HSA investors, their primary strength is their transaction fluidity. They allow for precise dollar-cost averaging down to the exact penny.

If your bi-weekly payroll contribution results in $169.23 sweeping into your account, an index mutual fund can absorb that exact amount, purchasing fractional shares automatically. This prevents uninvested cash balances from accumulating in your account.

Exchange-Traded Funds (ETFs)

ETFs trade throughout the day on the open market like individual stocks. They are famously lauded for their structural tax efficiency in regular accounts because they utilize “in-kind” creation and redemption mechanisms to avoid triggering capital gains distributions.

However, inside an HSA, this inherent tax benefit is neutralized because capital gains are already tax-sheltered. ETFs remain highly compelling for HSA investors whose platform allows fractional ETF trading (like Fidelity) or for those executing large, lump-sum annual transfers where real-time market pricing is preferred.

Target-Date Funds (TDFs)

Target-Date Funds represent an all-in-one, “set-it-and-forget-it” framework. You select a fund named after your projected retirement year (e.g., Vanguard Target Retirement 2050 Fund). The fund begins heavily weighted in aggressive equities and automatically shifts its allocation toward defensive bonds and cash as you approach that target year.

Crucial Warning: If you opt for a Target-Date Fund, ensure it is an index-based TDF (such as the Vanguard Target Retirement series or the Fidelity Freedom Index series). Avoid actively managed target-date iterations, which regularly carry inflated expense ratios exceeding 0.60%, silently draining your long-term returns.

Sample HSA Investment Strategies by Age and Risk Tolerance

Your strategic asset allocation should align with your age, investment timeline, and whether you intend to use the account for current medical bills or preserve it entirely for retirement. Below are three model allocation archetypes.

Strategy 1: The Aggressive Accumulator (Ages 20–39)

- Profile: Long investment horizon (20+ years). Healthy, with minimal ongoing medical obligations. Intends to pay current out-of-pocket healthcare costs using regular cash flow to maximize tax-free compounding.

- Target Allocation: 100% Equities

- Portfolio Blueprint:

- 75% Domestic Total Stock Market Index Fund (e.g., VTI or FSKAX)

- 25% Total International Stock Index Fund (e.g., VXUS)

How to Invest in the S&P 500: The Definitive Step-by-Step Guide

Strategy 2: The Balanced Wealth Builder (Ages 40–54)

- Profile: Mid-career phase. Developing a moderate baseline of medical expenses (e.g., family dental, pediatric visits). Balancing long-term capital appreciation with defensive risk mitigation.

- Target Allocation: 80% Equities / 20% Fixed Income

- Portfolio Blueprint:

- 60% U.S. Large-Cap Index Fund (e.g., FXAIX or VOO)

- 20% International Stock Index Fund (e.g., FSPSX or VXUS)

- 20% Core U.S. Bond Index Fund (e.g., FXNAX or BND)

Strategy 3: The Near-Retirement Conservator (Ages 55–65+)

- Profile: Preparing to transition into retirement within the decade. Seeking to preserve accumulated capital to fund upcoming healthcare needs while utilizing the age 55+ $1,000 catch-up contribution.

- Target Allocation: 50% Equities / 40% Fixed Income / 10% Cash

- Portfolio Blueprint:

- 40% S&P 500 Index Fund (e.g., SWPPX)

- 10% International Index Fund (e.g., VXUS)

- 40% Broad Market Bond Fund (e.g., BND)

- 10% Liquid Cash Buffer (held in the HSA’s core cash tier to absorb immediate deductibles)

Common Mistakes HSA Investors Make

Navigating an HSA requires avoiding several common operational pitfalls that can inadvertently trigger tax penalties or lead to significant opportunity costs.

Leaving the Account in Cash (The Inflation Trap)

According to extensive industry data compiled by Morningstar, less than 10% of HSA owners choose to invest their balances in the financial markets. The remaining 90%+ keep their entire balance sitting in the default cash interest tier, which often pays nominal yields under 0.10%.

When accounting for inflation, keeping long-term money in cash guarantees a loss of purchasing power over time. If you do not expect to use these funds for immediate, catastrophic medical bills, keeping them uninvested is a massive financial misstep.

Failing to Maintain a Meticulous Digital Receipt Archive

If you practice the advanced “shoebox strategy,” your primary point of failure is recordkeeping. If you claim a tax-free withdrawal 20 years from now based on a medical event that occurred today, you must be able to produce the itemized receipt in the event of an IRS audit.

Failing to preserve clean records can result in the IRS reclassifying your withdrawal as non-qualified, hitting you with ordinary income taxes plus a costly 20% penalty.

Relying on Direct Contributions over Payroll Deductions

While you can contribute to an HSA by manually transferring money from your personal bank account and claiming the deduction on your tax return, you miss out on a major tax break by doing so.

Whenever possible, coordinate with your employer’s HR department to set up automated payroll allocations. Direct deductions bypass the 7.65% FICA payroll tax completely. Direct manual contributions do not receive a refund for FICA taxes; they only reduce federal and state income taxes.

Expert Tips to Maximize Long-Term HSA Growth

- Establish a Digital Backup System: Use a secure cloud storage solution (like Google Drive, Dropbox, or a specialized financial vault) to scan and organize every medical invoice, Explanation of Benefits (EOB), and payment confirmation. Organize folders by calendar year to make future long-term claims simple.

- Utilize Spousal Catch-Up Rules: If both you and your spouse are age 55 or older and enrolled under a family HDHP, you can both contribute an extra $1,000 catch-up allocation. However, the IRS dictates that the second $1,000 catch-up allocation cannot be deposited into the main family HSA account. The spouse must open an independent, separate HSA account to house their individual catch-up contribution.

- Beware of State-Level Tax Anomalies: While HSAs enjoy clean federal tax-exemption, state-level tax codes can differ. For instance, California and New Jersey do not recognize the tax-exempt status of HSAs for state income tax purposes. If you reside in these states, your contributions are not deductible on your state return, and capital gains or dividends generated inside your HSA must be tracked and reported annually on your state tax filings.

Conclusion

Transitioning your health savings strategy from a simple short-term spending account to a disciplined investment vehicle is one of the most effective optimization strategies available in personal finance. The compounding value generated by the account’s unique triple tax advantage can form a substantial pillar of your retirement security.

Ultimately, finding the best HSA investment funds comes down to minimizing management expenses, maximizing broad market diversification, and matching your portfolio structure to your actual timeline for using the money. By anchoring your portfolio in institutional-grade index funds like FXAIX, VTI, or VOO and paying for immediate healthcare needs out of pocket, you turn routine medical savings into a powerful engine for building multi-generational wealth.

Frequently Asked Questions (FAQs)

Can I invest my HSA funds?

Yes, you absolutely can invest your HSA funds, provided your account custodian supports an investment platform. While almost all modern HSA providers offer an investment capability, many require you to cross a minimum cash balance threshold before you can move funds into mutual funds or ETFs. Once enabled, you can manage your holdings similarly to a traditional brokerage account or IRA.

Should I invest my HSA funds?

You should invest your HSA funds if you have stable cash flow, can afford to pay for your current out-of-pocket medical deductibles with regular income, and have a long-term retirement horizon. Investing allows you to maximize the account’s tax-free compounding potential. However, if you anticipate needing to spend your entire balance on medical bills over the next 12 to 24 months, you should keep those funds safe and liquid in cash rather than investing them in the stock market.

When can you invest HSA funds?

You can invest your HSA funds as soon as your account balance exceeds the minimum cash reserve requirement established by your administrator (often ranging from $0 to $2,000). Once your clear, settled contributions cross this threshold, you can manually or automatically sweep those excess dollars into your chosen investment options.

How to invest HSA funds?

To invest HSA funds, log in to your account provider’s online portal and locate the “Investment Options” or “Investment Sweep” tab. From there, you can choose to establish an automatic sweep rule that moves any future deposits exceeding your cash threshold directly into the market. Next, select your asset allocation from the provider’s fund lineup or open a linked self-directed brokerage window to purchase individual index mutual funds or ETFs.

Where to invest HSA funds?

If your employer specifies a mandatory provider, you must initially house your funds there to secure payroll tax advantages. However, if you are selecting a retail HSA independently, the best places to invest are low-cost brokerages like Fidelity or Charles Schwab. These platforms offer robust menus of top-tier index funds, institutional ETFs, fraction-share capabilities, and $0 ongoing account maintenance fees.

Best way to invest HSA funds?

The best way to invest HSA funds is to keep the architecture simple, low-cost, and passive. Build a resilient core portfolio utilising ultra-low-fee, broad-market index funds that trace the total U.S. stock market and global equity indexes. Minimise administrative cash drag, avoid expensive, actively managed mutual funds, and leave the capital untouched for decades to let the triple tax advantage work efficiently.