The financial sector has long preserved a clear hierarchy, and at its very apex sits the Investment Banker. To the outside observer, the profession is often viewed through a cinematic lens—a fast-paced world of sleek boardrooms, multi-billion-dollar mergers and acquisitions, and eye-catching year-end bonuses. Yet behind that polished image lies one of the most demanding careers in finance, requiring exceptional analytical ability, attention to detail, and the stamina to thrive under intense pressure.

An Investment Banker serves as a strategic advisor to corporations, governments, and institutions, helping them raise capital, navigate complex transactions, and execute major business deals. While the rewards can be substantial, success in the field comes from mastering financial modeling, valuation, negotiation, and client management rather than simply chasing large paychecks. The reality is that the profession combines intellectual rigor, structural complexity, and long working hours in a way that few careers can match.

To truly understand this domain, one must look past the superficial tropes and evaluate the mechanics of the system. Whether you are an aspiring finance professional mapping out your career, a corporate executive evaluating advisory options, or an investor tracking capital flows, understanding the machinery of high finance is essential.

Demystifying the Industry: What is Investment Banking?

Before looking at the day-to-day life of a senior dealmaker, we must answer a fundamental structural question: what is investment banking?

At its core, investment banking operates as a financial bridge connecting capital-seeking entities (corporations, governments, and institutional funds) with capital-providing entities (institutional investors, private equity groups, and public markets). Unlike standard commercial banks, which focus on collecting consumer deposits and issuing retail loans, an investment bank specializes in complex, large-scale financial strategies.

+-------------------------------------------------------------------+

| INVESTMENT BANK |

| |

| [ Capital Seekers ] ==========> [ Institutional Capital ] |

| - Corporations - Public Markets |

| - Sovereign Governments - Private Equity Funds |

| - Early-Stage Unicorns - Sovereign Wealth Funds |

+-------------------------------------------------------------------+

The industry generally splits its operations into two distinct areas:

- The Buy Side: Asset management firms, hedge funds, and private equity firms that deploy capital to purchase securities or acquire entire businesses.

- The Sell Side: Financial institutions that advise corporations on structural transactions, facilitate securities issuance, and execute market trades.

An institutional investment banker operates squarely on the sell side. They do not deploy their own capital to buy companies; instead, they serve as the strategic, legal, and financial architects behind major corporate transformations. When a global technology firm seeks to acquire a competitor, or an infrastructure giant intends to go public on the New York Stock Exchange, they hire these specialized intermediaries to value the assets, structure the legal frameworks, negotiate terms, and guarantee compliance with global financial regulations.

The Anatomy of a Dealmaker: Daily Roles and Responsibilities

The responsibilities of a professional in this field evolve dramatically based on corporate seniority. However, the overarching objective remains identical across all levels: flawless transaction execution.

The Analyst and Associate Layer (The Engine Room)

For junior execution professionals, the role is defined by quantitative data processing and material creation. The primary currency here is the pitchbook—a highly detailed presentation deck outlining market valuations, strategic acquisition targets, macroeconomic trends, and structural rationale for a potential corporate action.

A junior professional’s day consists of:

- Valuation Modeling: Constructing complex financial forecasts via Discounted Cash Flow ($DCF$) models, Leveraged Buyout ($LBO$) analyses, and Public Comps (Comparable Company Analysis).

- Due Diligence Coordination: Reviewing data rooms, auditing target company historical financial records, and identifying potential balance sheet liabilities during active transactions.

- Process Management: Coordinating with legal teams, forensic accountants, and regulatory bodies to ensure no procedural errors jeopardize a pending transaction.

The Vice President and Managing Director Layer (The Relationship Drivers)

As professionals climb the institutional ladder, their focus shifts from quantitative analysis to relationship management and origination. A Managing Director ($MD$) is fundamentally a corporate advisor and rainmaker. Their primary responsibility is to secure mandates—meaning they convince corporate boards and Chief Executive Officers to select their specific institution to lead upcoming equity offerings or M&A transactions. This requires deep industry relationships, an impeccable track record of successful executions, and a nuanced understanding of shifting macroeconomic conditions.

The Institutional Spectrum: From Bulge Brackets to Regional Players

The market for financial advisory services is highly segmented, ranging from massive global conglomerates down to specialized regional entities.

Bulge Bracket Investment Banks

At the top of the global league tables sit the bulge brackets. These are the massive, systemically important financial institutions that handle the largest, most visible corporate transactions in the world. Institutions like barclays investment bank, Goldman Sachs, and Morgan Stanley operate global networks spanning London, New York, Hong Kong, and Frankfurt.

These firms provide comprehensive financial services, including prime brokerage, global asset management, debt syndication, and sovereign advisory services. When a cross-border megadeal requires billions of dollars in committed bridge financing alongside complex multi-jurisdictional currency hedging, global corporations turn to these institutions due to their immense balance sheets and global placement power.

Elite and Regional Boutiques

Directly competing with the bulge brackets for pure advisory mandates are elite boutiques (such as Lazard, Evercore, and Centerview Partners). These firms focus strictly on financial advisory and M&A, consciously avoiding commercial lending or capital market underwriting.

Further down the asset spectrum are regional banks and middle-market advisory boutiques. While a global titan structures multi-billion dollar cross-border combinations, regional commercial institutions—such as investar bank—focus on providing essential commercial credit, localized corporate banking, and mid-market treasury solutions to small and mid-sized enterprises within specific geographical economic corridors. This multi-layered ecosystem ensures that whether a business is a mid-market manufacturing firm in the American South or a multinational energy conglomerate, appropriate financial advice and credit structures remain accessible.

Should You Buy Stock at All Time High? (The Truth Will Surprise You)

Deconstructing Financial Rewards: Salary and Wage Realities

One of the most intensely discussed topics surrounding high finance is professional compensation. The pay structure on Wall Street is uniquely incentivized, tying individual earnings directly to institutional performance and successful transaction flow.

The Multi-Tiered Pay Structure

An investment banker salary consists of two separate components: a fixed base salary and a variable year-end performance bonus. The bonus portion is highly volatile; in a booming market with rampant deal activity, a professional’s bonus can easily match or exceed their base pay. Conversely, during an economic contraction or market freeze, bonuses can drop significantly.

According to compensation tracking data across major corporate finance hubs, typical compensation structures generally align with the following ranges:

| Professional Rank | Average Base Salary | Expected Year-End Bonus | Total Annual Compensation |

| First-Year Analyst | $100,000 – $120,000 | $40,000 – $70,000 | $140,000 – $190,000 |

| Third-Year Associate | $175,000 – $225,000 | $100,000 – $200,000 | $275,000 – $425,000 |

| Vice President (VP) | $250,000 – $350,000 | $200,000 – $400,000 | $450,000 – $750,000 |

| Managing Director (MD) | $400,000 – $600,000+ | $500,000 – $2,000,000+ | $1,000,000 – $3,000,000+ |

The Actual Hourly Wage Reality

While these total compensation figures appear exceptionally high, they must be analyzed alongside the actual labor output required. Junior professionals regularly log between 80 to 90 hours per week, with peak deal environments pushing that figure past 100 hours. The concept of the “90-hour work week” is not a myth; it involves working from 9:00 AM to 2:00 AM consecutive days, alongside weekend modeling assignments.

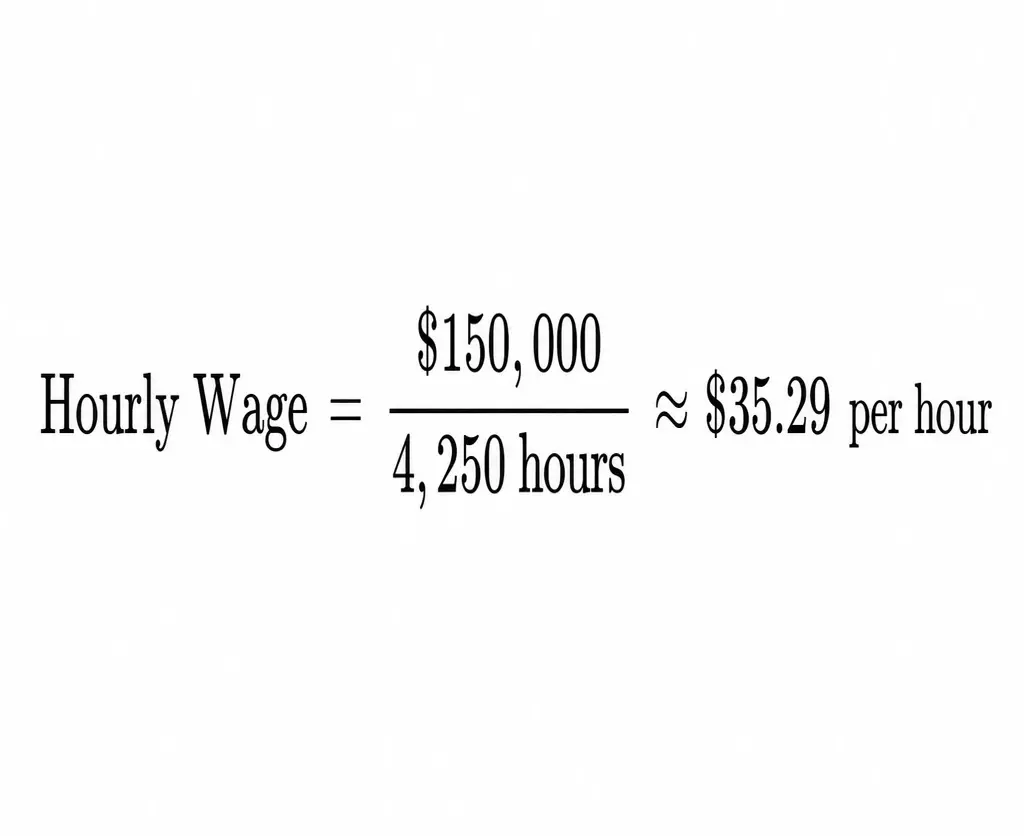

When you deconstruct this schedule to calculate the baseline investment banker wage on an hourly basis, the numbers present a much more grounded perspective. A first-year analyst earning a total of $150,000 while working 85 hours a week for 50 weeks puts in roughly 4,250 hours of highly intense labor per year.

This calculation highlights the reality of entry-level finance roles: the initial compensation is not high because of an astronomical hourly rate, but rather because of the sheer concentration of high-skill hours packed into a single calendar year. It operates as an intense corporate apprenticeship where professionals trade short-term work-life balance for long-term career optionality and financial upside.

Market Dynamics: Current Investment Banking News and Trends

The dealmaking environment is highly sensitive to macroeconomic shifts, monetary policy revisions, and broader technological disruptions. Staying informed on current investment banking news is critical for anticipating where institutional capital will flow next.

The AI Capital Expenditure Supercycle

Analysis of global deal data shows that corporate transaction structures are entering an historic innovation supercycle. The massive corporate urgency surrounding artificial intelligence has shifted from theoretical software experimentation to immense physical infrastructure consolidation. According to the latest Morgan Stanley M&A Intelligence Insights, corporate boards are actively using strategic acquisitions to close immediate capability gaps in compute capacity, fiber infrastructure, and green power grids.

This trend has triggered substantial deal flow in sectors that were previously considered slow-moving:

- Data Center Real Estate: Multi-billion dollar consolidation plays as institutional asset managers secure sites with pre-allocated power grid access.

- Industrial Cooling Equipment: Strategic acquisitions of advanced HVAC and liquid-cooling hardware providers by large industrial conglomerates rushing to support high-density AI servers.

- Semiconductor Intellectual Property: Mid-cap hardware designers being absorbed by tier-one tech players looking to insulate their supply chains against geopolitical friction.

The Private Credit Structural Disruption

Another major trend reshaping corporate finance is the rapid expansion of the private credit market. Historically, when an investment bank advised a private equity sponsor on a leveraged buyout, the bank would underwrite a massive syndicated loan, slice it up, and sell it to public debt markets or institutional bond investors.

As highlighted by the PwC Global Financial Services Deal Trends Report, private direct lenders have evolved into formidable institutional alternatives to traditional bank syndicates. Direct lending funds can now independently commit billions of dollars to a single corporate transaction, offering private structures, faster execution timelines, and floating-rate terms that avoid public market volatility entirely. As a result, bulge brackets are increasingly forming strategic joint ventures with private debt funds—fundamentally blurring the traditional lines between public capital markets and private credit deployment.

Navigating the Pipeline: Securing Investment Banking Jobs

Because the industry offers clear paths to executive leadership and highly lucrative exit options, securing an entry-level position remains incredibly competitive. Elite financial institutions routinely see thousands of Ivy League and top-tier business school applicants vying for a handful of analyst slots.

The Recruiting Lifecycle

The path to securing investment banking jobs begins long before graduation. The industry relies heavily on its structured Summer Analyst internship programs to fill its full-time incoming classes.

- Sophomore Year: Candidates focus on early networking, maintaining flawless grade point averages, and securing initial finance internships at regional institutions or boutique advisory shops.

- Junior Year (The Window): Active recruitment for summer analyst positions now initiates nearly a full year in advance. Elite institutions open applications and conduct structured technical interviews during the spring semester of sophomore year and the early fall of junior year.

- The Internship: A grueling 10-week summer internship serves as an extended, real-time interview. Interns who demonstrate flawless attention to detail, strong financial modeling skills, and strong cultural alignment are rewarded with full-time return offers upon graduation.

Essential Technical Skill Frameworks

To survive the rigorous interview process, a candidate must demonstrate an intuitive grasp of corporate accounting and valuation frameworks. The technical screening process evaluates more than rote memorization; it tests a candidate’s conceptual understanding of financial statements. A typical candidate must fluidly explain:

- How a $10 depreciation expense flows through the Income Statement, Cash Flow Statement, and Balance Sheet simultaneously.

- The economic trade-offs of financing a corporate acquisition through high-yield debt issuance versus equity dilution under varying interest rate environments.

- Why a company’s Enterprise Value ($EV$) remains theoretically unchanged regardless of whether it alters its capital structure via debt recapitalization or equity retirement.

+-------------------------------------------------------------+

| CORE TECHNICAL INTERVIEW PILLARS |

| |

| [ Accounting Fundamentals ] [ Valuation Methodologies ] |

| - Three-Statement Interlinks - DCF, LBO, and Public Comps |

| - Working Capital Dynamics - Enterprise Value Theory |

+-------------------------------------------------------------+

The “Airport Test”

Beyond raw quantitative skill, the final hurdle in corporate finance recruiting is behavioral alignment—frequently referred to by industry practitioners as the “airport test.” Senior dealmakers interviewing candidates ask themselves a simple qualitative question: “If our flight is delayed for five hours at an airport in Chicago during a winter storm, can I stand being stuck in a room talking to this person?” Because teams spend long nights together in deal war rooms under high stress, clear communication, emotional intelligence, and interpersonal adaptability are just as vital as mathematical precision.

Frequently Asked Questions (FAQ)

What is the difference between an investment banker and a private equity investor?

The core distinction lies in execution vs. ownership. An investment banker operates as a transaction advisor on the sell side; they are hired by a client to value a business, build marketing materials, coordinate negotiations, and execute a corporate sale or public offering. Once the transaction closes, the bank collects its advisory fee and exits the process.

Conversely, a private equity investor operates on the buy side; they deploy pooled institutional capital to buy a controlling stake in a business, take over operational oversight, optimize internal efficiencies over a five-to-seven-year investment horizon, and then sell the company later to generate returns for their limited partners.

Why do corporations pay investment banks such high fees for advisory services?

Corporations pay significant advisory fees—often calculated as a percentage of the total transaction value—because a major corporate transaction carries substantial execution, financial, and legal risks. A poorly structured multi-billion-dollar acquisition can easily destroy shareholder value, invite class-action litigation, or trigger antitrust blockages by regulatory bodies.

By hiring an elite advisory institution, a corporate board secures specialized valuation modeling, global market intelligence, extensive counterparty networks, and a vital structural buffer. This alignment of interests helps ensure that the strategic transaction is completed efficiently while maximizing shareholder value.

How has artificial intelligence impacted the day-to-day work of junior analysts?

According to insights published in the Harvard Law School Forum on Corporate Governance, artificial intelligence tools are actively automating the highly repetitive, manual aspects of entry-level finance roles. Tasks that historically required hours of manual data entry—such as spreading public company financial statements into Excel sheets, formatting pitchbook graphics, or aggregating initial industry research reports—are now executed rapidly by specialized enterprise AI platforms.

However, this shift has not eliminated the need for junior talent; instead, it has raised expectations. Modern junior professionals are expected to move past basic data aggregation and focus on higher-level analytical tracking, strategic model interpretation, and identifying complex data anomalies early in the transaction process.

Do you need an Ivy League degree to secure a job in investment banking?

While graduation from an elite target institution (such as Wharton, Harvard, NYU, or the London School of Economics) provides a clear advantage due to structured on-campus recruiting pipelines and extensive alumni networks, it is absolutely possible to enter the field from a non-target university.

Candidates from non-traditional backgrounds must approach the industry with a proactive strategy: building connections through cold outreach on professional networks, maintaining a flawless academic track record, securing early boutique finance internships, and demonstrating absolute mastery of complex valuation mechanics during technical interviews.

What are the standard exit opportunities after completing a junior banking analyst program?

Completing a two-year analyst stint at a reputable investment bank is highly valued across the corporate world because it serves as an intense professional boot camp. The most common exit pathways include moving to institutional buy-side firms like private equity funds, hedge funds, or venture capital groups. Alternatively, many analysts choose to move into corporate development roles within large enterprises, where they manage internal corporate acquisitions and strategic joint ventures from the corporate side. Others leverage their experience to launch venture-backed startups or pursue MBAs at elite business schools.