Let’s be honest about something right out of the gate: talking about money is usually uncomfortable. Most of us never received a formal education in managing personal finances. We graduated high school, maybe went to college, landed a job, and were suddenly expected to know how to navigate 401(k) allocations, decipher credit card terms, and magically build wealth.

That is exactly why Personal Finance Tips for Beginners are so valuable. Financial success is rarely about knowing complex investment strategies from day one. More often, it comes from understanding a few fundamental principles, building good habits, and making consistent decisions over time. The good news is that personal finance is a skill you can learn, regardless of your current income, age, or financial situation.

If you feel completely overwhelmed by your bank accounts, you are definitely not alone. In fact, one of the most common reasons people search for Personal Finance Tips for Beginners is because managing money can feel confusing, stressful, and overly complicated at first. Between checking accounts, savings goals, credit cards, loans, and investments, it is easy to feel like there is too much information to process.

The financial industry loves to make things sound complicated. They use jargon that makes investing and saving feel like an exclusive club where nobody has given you the password. But the truth is much simpler. One of the most valuable Personal Finance Tips for Beginners is understanding that successful money management does not require an MBA, a finance degree, or years of experience on Wall Street.

In reality, building wealth usually comes down to a handful of core habits practiced consistently over time. Spending less than you earn, avoiding unnecessary debt, saving regularly, and investing for the long term are far more important than mastering complex financial theories. The sooner you focus on these fundamentals, the easier it becomes to take control of your financial future.

Whether you are fresh out of college navigating your first real paycheck, or you are in your thirties realizing you need to get serious about the future, building a solid financial foundation starts right here.

Here are 10 essential personal finance tips for beginners that actually work.

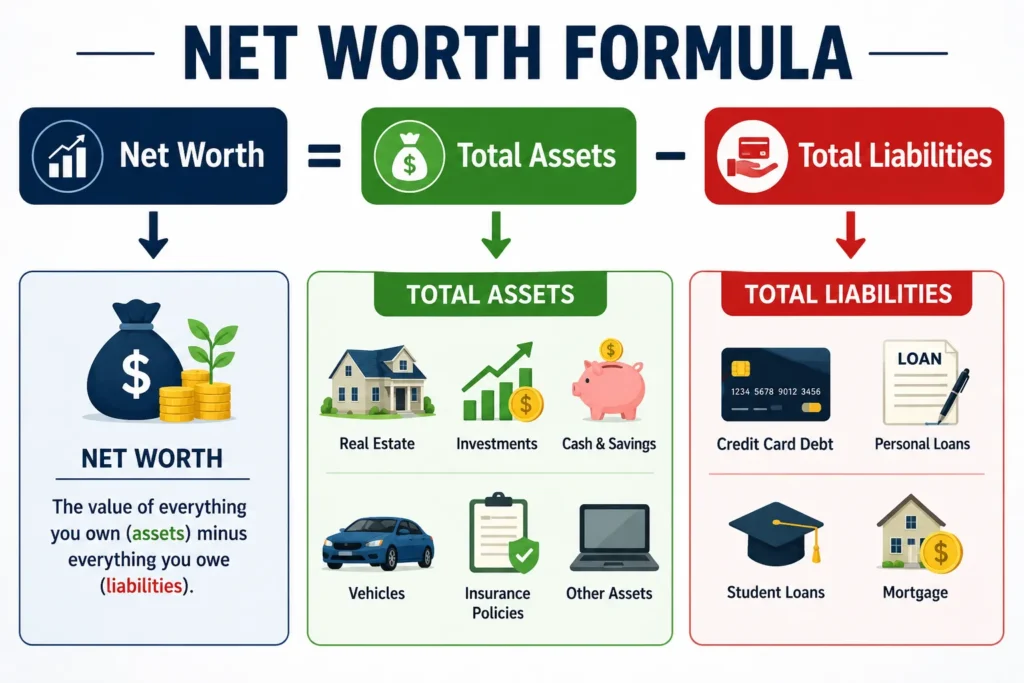

Face Your Financial Reality: One of the Most Important Personal Finance Tips for Beginners (Calculate Your Net Worth)

Before you can figure out how to get to your financial destination, you need to know exactly where you are standing today. This is one of the most important Personal Finance Tips for Beginners because every financial plan starts with understanding your current situation. It is incredibly common to avoid checking bank balances, reviewing credit card statements, or calculating debt totals because doing so can create anxiety and discomfort.

Your first step is to calculate your net worth. Among all Personal Finance Tips for Beginners, this is one of the most important because it gives you a clear snapshot of your overall financial health. Don’t let the term intimidate you—it sounds more complicated than it actually is.

Sit down with a cup of coffee, open a spreadsheet or grab a notebook, and list everything out.

| Assets (What You Own) | Liabilities (What You Owe) |

| Checking Account Balance | Credit Card Balances |

| Savings Account Balance | Student Loans |

| Retirement Accounts (401k, IRA) | Auto Loans |

| Value of your car via Kelley Blue Book | Personal Loans |

| Any investment accounts | Mortgage (if applicable) |

| Total Assets | Total Liabilities |

If that final number is negative, do not panic. It is completely normal for beginners, especially those carrying student loan debt, to have a negative net worth. The goal of this exercise isn’t to make you feel bad. It is to establish a baseline so you can track your progress month over month. For a deeper dive into adjusting your asset values, check out Investopedia’s comprehensive guide on calculating net worth. What gets measured gets managed.

2. Adopt the 50/30/20 Budgeting Framework

One of the most practical Personal Finance Tips for Beginners is to stop thinking of a budget as a restriction and start thinking of it as a spending plan. You are simply deciding in advance where your money will go instead of wondering where it went after it is already spent. In other words, you are giving every dollar a job before it hits your account. This approach creates clarity, reduces financial stress, and helps ensure your spending aligns with your goals and priorities.

For beginners, the 50/30/20 rule is the perfect starting point because it offers structure without micromanagement. Originally popularized by Senator Elizabeth Warren, you can track this layout using NerdWallet’s 50/30/20 budget framework. Here is how you split your after-tax income (your take-home pay):

- 50% for Needs: The non-negotiables. Rent or mortgage, groceries, utilities, basic transportation, minimum debt payments, and essential insurance.

- 30% for Wants: The fun stuff. Dining out, Netflix subscriptions, concert tickets, vacations, hobbies, and shopping for things you don’t strictly need to survive.

- 20% for Savings and Investing: Your future self. This bucket goes toward building your emergency fund, making extra payments on toxic debt, and investing for retirement.

Let’s look at a quick example:

Imagine your after-tax take-home pay is $4,000 a month.

- Needs (50%): $2,000

- Wants (30%): $1,200

- Savings (20%): $800

If you discover that your “Needs” category is consuming 70% of your income, that insight alone can be incredibly valuable. One of the most important Personal Finance Tips for Beginners is learning to identify financial imbalances before they become long-term problems. When essential expenses take up such a large portion of your earnings, you immediately know where your attention needs to go.

3. Build a “Sleep At Night” Emergency Fund

That is why building an emergency fund is consistently included among the most important Personal Finance Tips for Beginners. An emergency fund acts as a financial safety net, helping you cover unexpected expenses without relying on high-interest credit cards or taking on additional debt. Even a modest emergency fund can provide peace of mind and protect the progress you have worked hard to achieve. The goal is not to predict every problem—it is to be financially prepared when life inevitably throws one your way.

If you are relying on a credit card to cover emergencies, you are just turning a bad situation into a long-term financial drain through interest charges.

“Save for a rainy day, because it will rain.” — Traditional financial wisdom that never goes out of style.

The Action Plan:

- Phase One: The Starter Fund. Stop everything else and save $1,000 to $2,000 as fast as you can. Keep this in a high-yield savings account separate from your checking account so you aren’t tempted to spend it. This small buffer will cover 80% of minor everyday emergencies.

- Phase Two: The Fully Funded Reserve. Once your high-interest consumer debt is paid off (more on that next), build this fund until it can cover 3 to 6 months of your essential living expenses (that 50% category from your budget).

Expert Personal Finance Tips to Help You Build Long-Term Wealth

4. Declare War on High-Interest Debt

Not all debt is created equal. A mortgage with a 4% interest rate is vastly different from a credit card charging 24% interest. One of the most important Money Management Tips is learning to distinguish between manageable debt and debt that actively works against your financial future.

High-interest consumer debt is a serious wealth destroyer because it compounds against you every single month. While investments can help your money grow over time, high-interest debt can erase those gains just as quickly. That is why effective Money Management Tips almost always prioritize paying off high-interest credit card balances before focusing on aggressive investing. If you are carrying expensive consumer debt, treat it as a financial emergency and create a plan to eliminate it as quickly as possible.

When you carry a balance on a credit card charging 20% or more in annual interest, you are effectively paying a steep penalty for purchases that were not covered with cash. One of the most valuable Money Management Tips is understanding the true cost of high-interest debt. What may seem like a manageable balance can quickly grow as interest charges accumulate month after month.

There are two primary psychological strategies for destroying debt, which are evaluated structurally in the Investopedia Debt Avalanche vs. Debt Snowball comparison:

- The Debt Snowball (Momentum Focus): You list all your debts from the smallest balance to the largest balance, regardless of the interest rate. You pay minimums on everything, but throw every extra dollar at the smallest balance until it’s gone. Then, you take that payment and roll it into the next smallest. This method provides quick psychological wins that keep you motivated.

- The Debt Avalanche (Math Focus): You list your debts from the highest interest rate to the lowest interest rate. You attack the highest interest rate first. Mathematically, this saves you the most money over time, but it can take longer to get that satisfying feeling of wiping out a complete account.

Pick the approach that best matches your personality and motivates you to stay consistent. One of the most practical Money Management Tips is recognizing that the perfect strategy on paper is useless if you cannot stick with it long enough to see results.

5. Automate Everything You Can

Human beings are naturally flawed when it comes to discipline. If you have to actively make the choice to log into your bank account and transfer money to savings every single payday, you are eventually going to slip up. You’ll convince yourself that you just need the cash this month, and you’ll save double next month. (Spoiler: Next month never happens).

This is why automation is one of the most effective Money Management Tips available. By setting up automatic transfers to your savings account, retirement fund, or investment account, you remove the need to make the same decision over and over again. Instead of relying on willpower, you create a system that works in the background and keeps your financial goals moving forward.

The secret to building wealth more easily is removing as much dependence on willpower as possible. One of the most effective Money Management Tips is to create systems that make good financial decisions happen automatically. Willpower is limited, especially when life gets busy or unexpected expenses arise.

- Automate your savings: Set up a recurring transfer so that the day your paycheck hits your checking account, 20% is immediately funneled into your savings or investment accounts. Treat it like a tax. If you never see the money, you won’t miss it.

- Automate your bills: Put your utilities, minimum debt payments, and subscriptions on auto-pay. This guarantees you will never pay a late fee or take a hit to your credit score because you simply forgot what day it was.

6. Maximize Your Employer Match (Grab the Free Money)

If you work for a company that offers a 401(k) or similar workplace retirement plan, one of the most valuable Personal Finance Tips for Beginners is to find out immediately whether your employer provides a matching contribution. An employer match is essentially additional money added to your retirement account based on your own contributions.

An employer match is exactly what it sounds like: your company will match your retirement contributions up to a certain percentage of your salary. For example, a common structure is a 100% match on the first 3% of your salary you contribute, and a 50% match on the next 2%.

If your company offers a match and you are not contributing enough to get the full amount, you are voluntarily taking a pay cut. To check the legal contribution ceilings for the current tax year, refer to the IRS 401(k) Contribution Limits.

Let’s say you make $60,000 a year, and your company matches 100% up to 5%.

- If you contribute 5% ($3,000 a year).

- Your employer also puts in $3,000.

That is a guaranteed, immediate 100% return on your investment. There is nowhere else in the financial world where you can get a guaranteed 100% return safely. Even if you are aggressively paying down debt, you should generally contribute exactly enough to get your full employer match. It is literally free money.

7. Understand and Protect Your Credit Score

Your credit score is essentially your adult GPA. It dictates so much more than just whether you can get a credit card. Your FICO score impacts your ability to rent an apartment, the rates you pay for auto insurance, whether you need to put down massive deposits for utilities, and most importantly, the interest rate you will get on large purchases like a home or a car.

A small difference in an interest rate on a 30-year mortgage can mean a difference of tens of thousands of dollars over the life of the loan. For details on your federal consumer rights regarding credit reporting, you can explore the Consumer Financial Protection Bureau (CFPB) Credit Guide.

How your FICO score is calculated:

| Factor | Weight | What It Means For You |

| Payment History | 35% | Pay your bills on time, every time. A single missed payment can tank your score. |

| Amounts Owed | 30% | This is “Credit Utilization.” If you have a $10,000 credit limit, try to keep your balance under $3,000 (30%). Lower is better. |

| Length of History | 15% | Don’t close your oldest credit card account, even if you rarely use it. History matters. |

| New Credit | 10% | Don’t apply for 5 store credit cards in a single month. It makes you look desperate for cash. |

| Credit Mix | 10% | Having a mix of revolving (credit cards) and installment (auto loans) debt. Don’t worry too much about this as a beginner. |

Pro Tip: You are legally entitled to free credit reports from the major bureaus atAnnualCreditReport.com. Check them annually to ensure there are no errors or fraudulent accounts in your name.

8. Start Investing Yesterday (Keep It Boring)

A lot of beginners think keeping all their money in a traditional checking account is the safest thing they can do. It’s actually a guaranteed way to lose money.

Because of inflation (the rising cost of goods over time), money sitting under a mattress or in a checking account earning 0.01% is losing its purchasing power every single year. To build wealth, your money has to grow faster than inflation. That means you have to invest.

Investing doesn’t mean picking individual stocks, day trading on an app, or buying into the latest crypto hype. That is speculating, which is essentially gambling. Real wealth building is remarkably boring.

The Beginner’s Playbook for Investing:

- Open a Roth IRA: If you’ve gotten your employer match and paid off high-interest debt, open a Roth IRA (Individual Retirement Account). You fund it with after-tax money, it grows tax-free, and you can pull it out tax-free in retirement.

- Buy Low-Cost Index Funds or ETFs: Instead of trying to find the “next big thing,” buy a little piece of everything. An S&P 500 index fund allows you to own a tiny sliver of the 500 largest companies in the US. You can learn more about how these assets hold up long-term via Vanguard’s Index Investing Overview. As the overall economy grows, your money grows.

- Let Compound Interest Work: Time in the market always beats timing the market. The earlier you start putting money away, the more time your interest has to earn its own interest.

9. Beware the Trap of Lifestyle Creep

Have you ever noticed that the more money people make, the more they seem to struggle? This phenomenon is known as lifestyle creep, or Parkinson’s Law of Money: Expenses rise to meet income.

When you get your first major raise or promotion, the natural inclination is to upgrade your life immediately. You move into a luxury apartment building, trade in your reliable Honda for a luxury SUV, and start eating at upscale restaurants on Tuesdays. Suddenly, you are making $30,000 more a year, but you have less cash left over at the end of the month than you did before.

There is nothing wrong with enjoying the fruits of your labor. But to build actual wealth, you have to break the cycle of lifestyle creep.

The Fix: When you get a raise, allocate a specific percentage of the new money (say, 20%) to fun and lifestyle upgrades. Take the remaining 80% and immediately funnel it into your savings, investments, or debt payoff plans. You get to enjoy the raise, but your net worth grows exponentially.

10. Set Specific, Time-Bound Financial Goals

“I want to be rich” is not a financial goal. It is a vague wish. Without a clear target, you will drift aimlessly and likely fall prey to impulse spending.

To make progress, you need to apply the SMART framework to your money (Specific, Measurable, Achieved, Relevant, Time-bound). When your goals are crystal clear, it becomes much easier to say no to immediate gratification because you are saying yes to something you want more.

- Bad Goal: I want to save money for a house.

- Good Goal: I want to save $24,000 for a down payment on a home by saving $1,000 a month for the next 24 months, automatically transferred to a high-yield savings account on the 1st and 15th of every month.

Write your financial goals down. Put a sticky note on your computer monitor. Wrap a picture of your dream vacation around your credit card so you have to look at it before you swipe for something you don’t need. Keep the “why” front and center.

The Bottom Line

Personal finance isn’t about being perfectly frugal 100% of the time, and it isn’t about getting rich overnight. It is a marathon of consistency. It’s about building a gap between what you earn and what you spend, and intentionally deciding what to do with that gap.

Start small. Calculate your net worth this weekend. Set up one automated transfer to your savings account. Check your credit score. If you take these steps one by one, year over year, you’ll wake up a decade from now wondering why you were ever stressed about money in the first place. You have the tools. Now, go put them to work.

Frequently Asked Questions (FAQ)

What is a high-yield savings account (HYSA), and do I really need one?

A high-yield savings account is just a regular savings account that pays a significantly higher interest rate than standard traditional banks—often up to 10 to 12 times the national average. Keeping your emergency fund in a traditional checking or basic savings account means inflation is slowly eating away at its purchasing power. An HYSA keeps your cash liquid and accessible for sudden emergencies while allowing it to grow enough to counter rising everyday costs.

Should I pay off all my debt before I start investing for retirement?

Not necessarily. The general rule of thumb is to look at the interest rates. If your employer offers a matching 401(k) program, prioritize contributing just enough to grab that full match first—that is an instant 100% return on your money. After that, focus heavily on wiping out high-interest consumer debt (anything above 7-8%, like credit cards). If you have low-interest debt, like a predictable student loan or mortgage under 4-5%, you can comfortably invest for your future while paying the regular monthly minimums.

What should I do if my “Needs” take up way more than 50% of my income?

If you live in a high-cost-of-living area, your housing and utilities might easily consume 60% or 70% of your take-home pay. Don’t panic, and don’t abandon the system. The 50/30/20 framework is a flexible benchmark, not a law. In this situation, you must aggressively shrink your “Wants” column down to 10% or 15% to protect your 20% savings goal. Your baseline structure should temporarily shift to a 65/15/20 or 70/10/20 breakdown while you actively look for ways to decrease fixed overhead or negotiate a salary increase.

How often should I check my net worth and credit score?

Checking your net worth once a month during a regular financial check-in is ideal. Tracking it more frequently creates unnecessary anxiety over minor daily market fluctuations. For your credit score, monitoring it once a month via free dashboard tools is perfectly fine to ensure no unexpected drops occur. Additionally, make it a habit to pull your official, comprehensive credit reports annually to audit for any underlying errors or fraudulent background activity.

Is a Roth IRA or a Traditional 401(k) better for a beginner?

If your employer provides a 401(k) match, that is always your absolute starting point. Once you secure that match, a Roth IRA is an exceptional tool for beginners because it operates on a different tax logic. You fund a Roth IRA with money that has already been taxed today, allowing the investments to grow entirely tax-free. When you retire, you can withdraw that accumulated wealth without owing the government a single cent. It is an ideal setup if you expect your income and tax bracket to rise over the course of your career.