Let’s be entirely honest: most personal finance advice is incredibly dry. It reads like a washing machine manual written by an overcautious tax attorney. If your strategy for getting good with money consists of skipping your morning latte, clip-ops couponing, and staring miserably at a banking app, you are setting yourself up for financial and psychological burnout.

Real financial freedom doesn’t come from deprivation; it comes from changing the structural architecture of how you think about risk, time, and value. The absolute cheapest way to rewrite your financial script is to read the minds of the people who have already solved the puzzle.

Whether you are drowning in consumer debt, trying to build an investment portfolio from scratch in a shifting economy, or wondering how to navigate the modern high-interest landscape, here is the definitive guide to the personal finance books that actually move the needle.

The Psychological Foundations (The Mindset Shift)

You can know everything there is to know about index funds, tax codes, and compound interest. But if you don’t understand your own psychological triggers, you will still make catastrophic decisions with your money. Behavior always trumps math.

1. The Psychology of Money – Morgan Housel

If you only ever read one book on this list, make it this one. Housel, a former columnist for The Motley Fool and the Wall Street Journal, strips away the complex spreadsheets and looks at money through the lens of human history, ego, envy, and emotion.

- The Big Idea: Doing well with money isn’t necessarily about what you know. It’s about how you behave. And behavior is hard to teach, even to really smart people.

- The Core Framework: Housel introduces the concept that “no one is crazy.” Every person makes financial decisions based on the unique experiences they had during their formative years. If you grew up during times of hyperinflation, your investment strategy will look completely different from someone who grew up during an unprecedented bull market.

- Key Takeaway: True wealth is the things you don’t buy. It’s the expensive cars not purchased, the diamonds not worn, and the first-class tickets passed up. Wealth is option value; it’s the structural freedom to wake up in the morning and say, “I can do whatever I want today.”

2. Rich Dad Poor Dad – Robert Kiyosaki

This is arguably the most controversial book in the personal finance ecosystem. Many modern analytical economists dislike it because Kiyosaki’s specific real estate and tax claims can border on the legally hyper-aggressive. However, its core philosophical paradigm shift remains completely unmatched for beginners.

- The Big Idea: The poor and the middle class work for money. The rich have money work for them.

- The Structural Shift: Kiyosaki redefines what an asset actually is. Traditional accounting says your primary residence is your biggest asset. Kiyosaki completely dismantles this.

- The Golden Definition: If it takes money out of your pocket, it’s a liability. If it puts money into your pocket, it’s an asset. Under this definition, your heavily mortgaged home is a liability until the day you rent it out or sell it for a profit.

3. The Millionaire Next Door – Thomas J. Stanley & William D. Danko

This book is the ultimate reality check for the Instagram era. Based on decades of empirical research into real American millionaires, the authors discovered that the people with the highest net worths rarely live in luxury enclaves, drive exotic supercars, or wear haute couture.

- The Core Terminology: The authors divide the population into two distinct camps:

- UAWs (Under Accumulators of Wealth): High income, low net worth. They spend everything they make to maintain a luxurious facade.

- PAWs (Prodigious Accumulators of Wealth): Low or moderate spending relative to income, high net worth. They build real, invisible security.

- The Key Driver: Frugality and budgeting are the cornerstones of wealth building. The typical millionaire drives a reliable, used domestic car, lives in a middle-class neighborhood, and runs a mundane blue-collar business (like a dry cleaner or a welding shop).

The Tactical Frameworks (Automation & Cash Flow)

Once your mindset is cleared of consumerist programming, you need an actionable system. You need to know exactly which accounts to open, how to route your monthly paycheck, and how to spend money without guilt.

4. I Will Teach You To Be Rich – Ramit Sethi

Sethi’s approach is incredibly refreshing because he completely rejects the traditional personal finance trope of sacrifice. He explicitly tells you to keep buying your $6 lattes. Instead, he advocates for what he calls “Conscious Spending.”

[ Gross Monthly Income ]

│

▼

[ 1. Fixed Costs: 50-60% ]

(Rent, Utilities, Minimum Debt Payments)

│

┌────────────────┴────────────────┐

▼ ▼

[ 2. Investments: 10% ] [ 3. Savings Goals: 5-10% ]

(Index Funds, Retirement) (Holidays, Down Payments)

│ │

└────────────────┬────────────────┘

▼

[ 4. Guilt-Free Spending: 20-35% ]

(Dining Out, Luxury, Hobbies)

- The System: Sethi provides a highly detailed, 6-week program designed to fully automate your financial infrastructure. Once configured, your bills pay themselves, your retirement accounts are automatically funded, and whatever cash is left over in your checking account can be spent with absolutely zero psychological guilt.

- The Philosophy: Focus on the “Big Wins” (negotiating a salary raise, choosing the right investment mix, buying a reasonably priced home) rather than agonizing over minor expenses.

5. The Total Money Makeover – Dave Ramsey

Dave Ramsey is the drill sergeant of the personal finance world. His advice is rigid, emotionally driven, and highly effective for individuals who find themselves in deep consumer debt emergencies.

- The Baby Steps Framework:

- Step 1: Save a quick $1,000 beginner emergency fund.

- Step 2: Pay off all debt (except the house) using the Debt Snowball.

- Step 3: Build a fully funded 3 to 6-month emergency reserve.

- Step 4: Invest 15% of your household income into retirement.

- The Debt Snowball vs. Avalanche: Ramsey insists on the Snowball method—paying off your smallest debts first regardless of the interest rate. While mathematically sub-optimal compared to the Avalanche method (paying the highest interest rate first), it leverages human psychology by providing quick behavioral wins.

The Investing Masterclasses (Building Passive Wealth)

You cannot save your way to true financial independence. To beat systemic inflation, your money must grow exponentially while you sleep.

6. The Simple Path to Wealth – JL Collins

What originally started as a series of private letters written by a father to his young daughter turned into the ultimate manifesto for hands-off investing. Collins demystifies the financial services sector and champions a single, ultra-low-cost asset class.

- The Strategy: Avoid complex day trading, avoid actively managed mutual funds, and completely tune out the daily panic of financial news networks. Buy broad-market index funds (like VTSAX or VTI), hold them forever, and reinvest the dividends.

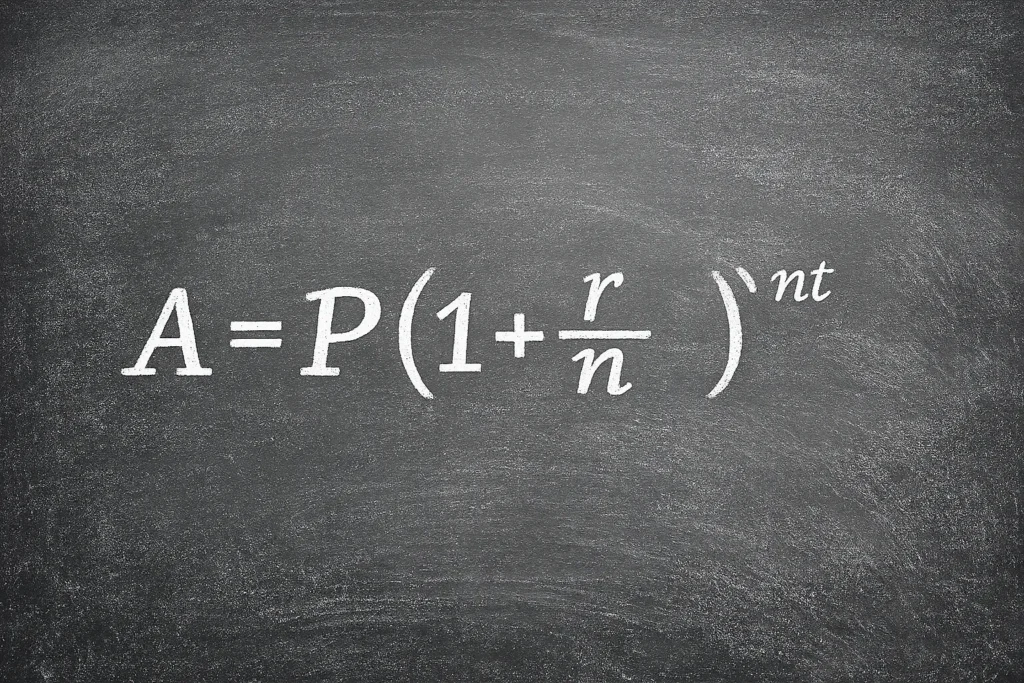

- The Foundation: Long-term equity wealth can be evaluated by the classic compounding formula:

Collins argues that instead of trying to manipulate $P$ through risky individual stock picking or trying to divine short-term adjustments to $r$, individual investors should simply capture the total return of the global economy over a long horizon ($t$).

The Book Selection Matrix: Match Your Goal to the Right Text

| Book Title | Core Financial Focus | Strategy Type | Difficulty | Best Match For… |

| The Psychology of Money | Behavioral Economics | Mindset Restructuring | Easy / Narrative | Breaking free from lifestyle inflation and toxic comparison cycles. |

| I Will Teach You To Be Rich | Cash Flow & Automation | Automated Checking/Savings | Moderate / Actionable | Setting up a zero-maintenance monthly banking pipeline. |

| The Simple Path to Wealth | Low-Cost Index Investing | Buy-and-Hold Vanguard Funds | Easy / Direct | Building an absolute hands-off retirement nest egg. |

| The Total Money Makeover | Severe Debt Liquidations | Debt Snowball Process | Easy / Rigid | Crushing high-interest credit card debt under immense pressure. |

| Your Money or Your Life | Financial Autonomy (FIRE) | Life Energy Calculations | Advanced / Analytical | Escaping the corporate rat race entirely by modifying lifestyle metrics. |

Lifestyle Design & The FI/RE Movement

Money is just a tool. If you accumulate millions of dollars but sacrifice your physical health, mental well-being, and relationships along the way, you have lost the game. These books focus on the ultimate prize: using currency to buy absolute time autonomy.

7. Your Money or Your Life – Vicki Robin & Joe Dominguez

The undisputed foundational blueprint of the FI/RE (Financial Independence, Retire Early) movement. This book forces you to calculate your “real hourly wage” by factoring in all the hidden costs of holding down a job.

- The Calculation: If you make $\$40$ an hour but spend two unpaid hours a day commuting, $\$50$ a week on dry cleaning, and hundreds on convenience meals because you’re too exhausted to cook, your real hourly compensation is drastically lower than your contract states.

- The Paradigm: Money is nothing more than something you trade your finite “life energy” for. If you view every consumer purchase through this lens—“Is this new couch worth 40 hours of my remaining life energy?”—your spending patterns naturally drop off a cliff.

8. Die with Zero – Bill Perkins

The perfect intellectual counter-weight to hyper-frugal minimalist finance books. Perkins argues that optimizing your life purely for maximum accumulation means dying with a bank account balance that represents wasted health and missed opportunities.

- The Argument: The utility of a dollar changes dramatically based on your physical age and health status. A dollar spent on a backpacking trip through Europe at age 25 yields decades of compounding “memory dividends.” That same dollar spent on a vacation at age 78, when your mobility may be severely compromised, has an incredibly low utility score.

- The Application: Learn to balance saving for your later years with intentionally spending your capital on peak experiences while you still have the physical health to fully enjoy them.

10 Essential Personal Finance Tips for Beginners

Advanced & Corporate Perspectives

For those who have already automated their personal cash flow, wiped out consumer liabilities, and established a base layer of index funds, it’s time to study how institutional wealth is protected and scaled.

9. Principles: Life and Work – Ray Dalio

Ray Dalio, the founder of Bridgewater Associates (the world’s largest hedge fund), shares the structural rules engine he developed to manage both his global investment portfolios and his corporate enterprise.

┌────────────────────────────────────────┐

│ 1. Identify Clear Goals │

└───────────────────┬────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ 2. Encounter Problems & Failures │

└───────────────────┬────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ 3. Diagnose the Root Causes │

└───────────────────┬────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ 4. Design a Corrective Plan │

└───────────────────┬────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ 5. Execute the Plan to Results │

└───────────────────┴────────────────────┘

- The Machine Analogy: Dalio views life and business as a series of interconnected machines. To optimize your personal economy, you must look down upon yourself objectively as an engineer looking at a system loop.

- The Financial Application: Radical truth and radical transparency help eliminate the emotional cognitive biases that cause retail investors to panic-sell during market corrections.

The Pitfalls & Scams (What Not to Read)

An essential part of building a world-class financial library is knowing which books to leave on the shelf. The modern publishing landscape is crowded with speculative trash masquerading as revolutionary financial insight.

How to Spot Financial Grift Culture:

- The “One Secret Trick” Promise: If a book claims to have a hidden loop that Wall Street doesn’t want you to know about, it is marketing snake oil.

- Hyper-Speculative Derivative Focus: Books that advocate for complex options trading, high-leverage forex strategies, or micro-cap crypto allocations as a sustainable way to build long-term generational wealth should be avoided entirely.

- The Real Estate Unlimited Leverage Loop: Be exceptionally careful with books written during historic low-interest-rate eras that tell you to borrow infinity dollars to buy run-down apartment buildings. In high-interest macroeconomic cycles, that strategy leads directly to bankruptcy.

Deep-Dive FAQ Section

Q: What is the single best personal finance book for absolute beginners?

A: Start with The Psychology of Money by Morgan Housel to repair your behavioral relationship with wealth. Follow it up immediately with I Will Teach You To Be Rich by Ramit Sethi for your concrete, step-by-step account configuration.

Q: Can reading books actually solve my debt crisis?

A: A book cannot physically cut a check to your creditors, but it can provide the psychological framework required to stop making bad choices. If you are struggling with severe debt, Dave Ramsey’s The Total Money Makeover provides an aggressive, psychological methodology to help you climb out of that situation.

Q: Is The Intelligent Investor by Benjamin Graham too outdated for today’s market?

A: The foundational concepts—like “Mr Market” and the “Margin of Safety”—remain timeless. However, the specific asset evaluations and corporate accounting examples from the mid-20th century can feel incredibly archaic to a modern retail investor. Read it for structural theory, not for day-to-day stock picking tactics.

Q: Should I read books written specifically for my country?

A: Mindset books (The Psychology of Money, Your Money or Your Life) are globally universal because human nature is identical everywhere. However, tactical books dealing with specific tax codes, retirement vehicles (like 401ks in the US, ISAs in the UK, or Superannuation in Australia), and real estate laws should be augmented by top-tier local authors. For example, Australian readers frequently lean on Scott Pape’s The Barefoot Investor for local structures.

The Step-by-Step Implementation Blueprint

Do not fall into the trap of financial voyeurism—reading book after book without changing a single setting in your real-life bank account. Use the One-Action Rule:

- Read a Chapter: Highlight the core tactical lesson.

- Pause the Book: Close the pages.

- Execute Immediately: Open your bank portal. Set up that automatic transfer, call your lender to negotiate an interest rate reduction, or open that index fund brokerage account.

- Resume: Move to the next book only when the previous book’s lessons are hardcoded into your financial life.

For real-time market updates, economic metrics, and data validation, consult specialized portals like Investopedia or the Bogleheads Wiki.