“We’ve all seen the headlines: ‘This 25-year-old saved $100k by living in a van and eating nothing but lentils.’ While that’s… impressive? It’s not exactly a sustainable lifestyle for most of us who enjoy things like indoor plumbing and a social life that doesn’t involve explaining why we smell like legumes. The truth is, good personal finance tips don’t have to involve extreme sacrifices — smart budgeting, mindful spending, and consistent saving can make a huge difference without giving up the life you enjoy.”

“The truth is, building long-term wealth isn’t about extreme deprivation. It’s about systems, psychology, and math. Most people treat their finances like a game of Whac-A-Mole—reacting to bills as they pop up. To move from ‘surviving’ to ‘wealthy,’ you have to stop playing defense and start playing offense. That’s why effective personal finance tips focus on building smart financial habits, long-term strategies, and consistent investing rather than short-term sacrifices.”

If you’re ready to move past the “beginner” stage of saving pennies and start building a fortress of wealth, here are the expert personal finance tips that actually move the needle.

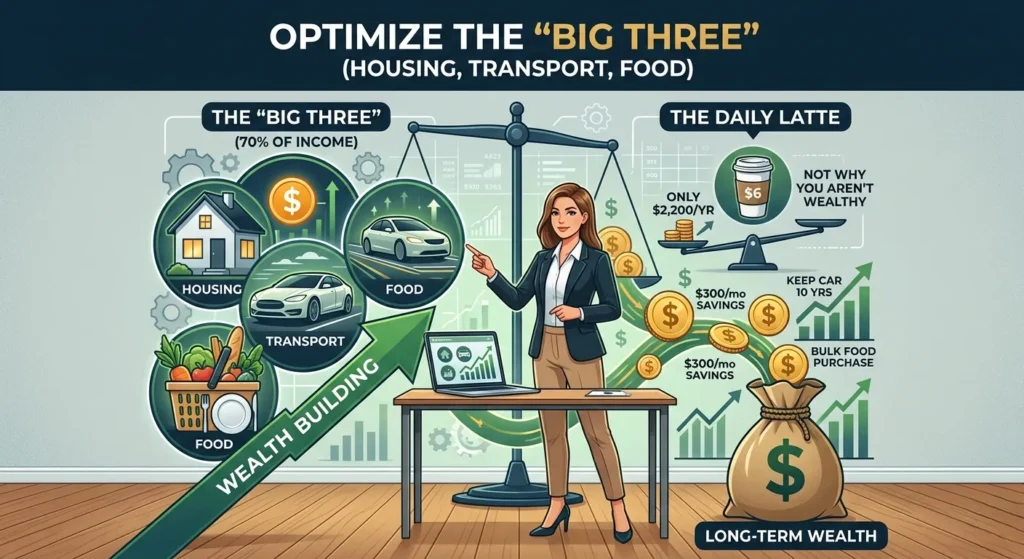

1. Optimize the “Big Three” (Housing, Transport, Food)

“Financial ‘gurus’ love to beat you over the head for buying a $6 latte. Let’s do the math: a daily $6 latte is about $2,200 a year. That’s not nothing, but it’s not why you aren’t wealthy. You aren’t wealthy because your ‘Big Three’ expenses—housing, transportation, and food—are eating 70% of your take-home pay. That’s why the best personal finance tips focus less on guilt-tripping small pleasures and more on managing the major expenses that truly impact your financial future.”

If you can reduce your rent by $300 a month by moving ten minutes further away, or keep your car for 10 years instead of 3, you’ve already saved more than five years’ worth of lattes.

The Wealth-Builder’s Target: Personal Finance Tips That Actually Work

- Housing: Keep it under 28% of your gross income.

- Transport: Buy used, pay cash if possible, and drive it until the wheels fall off.

- Food: Master the art of the “Bulk Prep” but don’t be afraid to dine out occasionally—just make it an intentional choice, not a “I’m too tired to cook” default.

2. Treat Your HSA Like a “Secret” IRA

“Most people think a Health Savings Account (HSA) is just a way to pay for bandages and prescriptions. Experts know it is the single most powerful investment vehicle in the American tax code. In fact, many underrated personal finance tips highlight HSAs as a smart long-term wealth-building tool, not just a medical expense account.”

An HSA offers a “triple tax advantage” that even a 401(k) can’t match:

- Tax-deductible contributions: You lower your taxable income today.

- Tax-free growth: Your investments grow without the IRS taking a cut.

- Tax-free withdrawals: As long as you use the money for medical expenses, you never pay taxes on it.

“The Expert Move: If you can afford to pay for your current medical expenses out of pocket, do it. Leave the money in the HSA, invest it in the S&P 500, and let it compound for 20 years. According to IRS Publication 969, once you hit age 65, you can withdraw the money for anything (though you’ll pay income tax on non-medical withdrawals, just like a traditional IRA). Among advanced personal finance tips, this strategy is often considered one of the smartest ways to maximize tax-free growth and long-term retirement savings.”

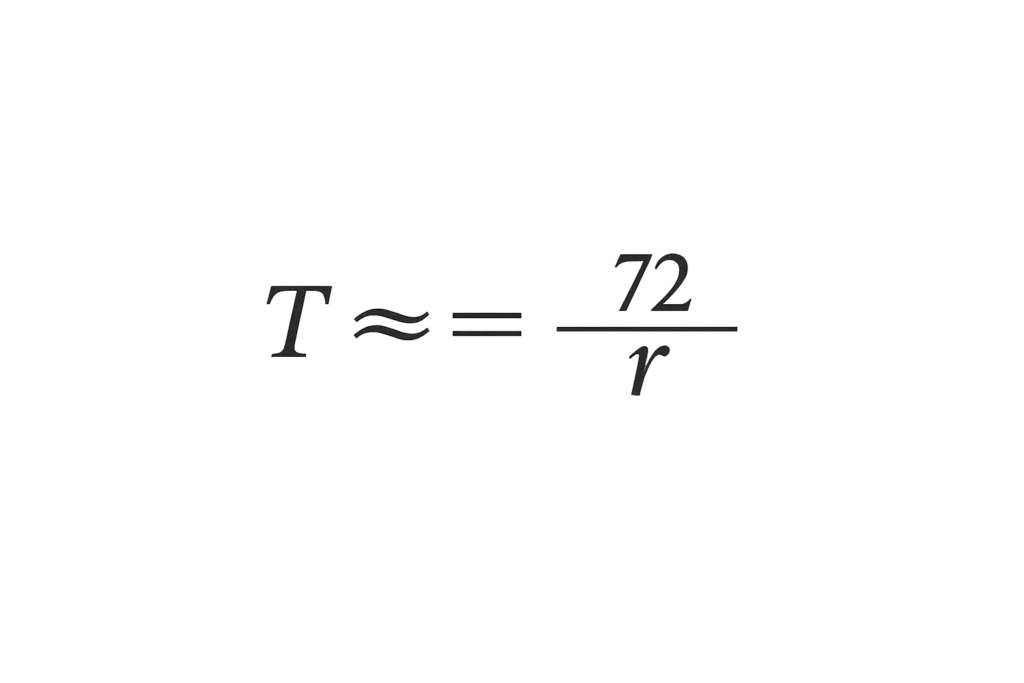

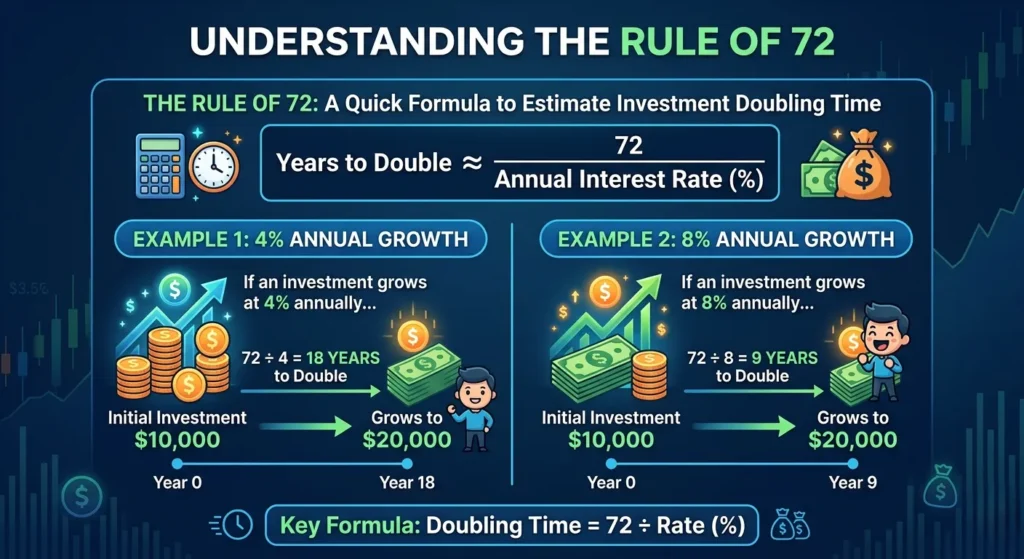

3. Understand the “Rule of 72” and the Cost of Waiting

“Wealth is a factor of time and rate of return. The ‘Rule of 72’ is a quick mental shortcut to see how long it will take for your money to double at a given interest rate. Among the most valuable personal finance tips, understanding compound growth and simple formulas like the Rule of 72 can help you make smarter long-term investment decisions.”

The formula is simple:

Where:

- $T$ = Time to double your money

- $r$ = Annual rate of return

“If you’re earning an 8% return on an index fund, your money doubles every 9 years ($72 / 8 = 9$). If you wait just one decade to start, you are missing out on at least one ‘double.’ On a $100,000 portfolio, that’s a $100,000 mistake. That’s why many personal finance tips emphasize starting early — because time in the market is often more powerful than trying to perfectly time the market.”

4. Eliminate the “Fee Parasites”

In the investing world, you get what you don’t pay for. Many “managed” mutual funds charge expense ratios of 1% or higher. That sounds small, but over a 30-year career, a 1% fee can eat nearly one-third of your total wealth.

Look at the difference in a $100,000 portfolio over 30 years with a 7% return:

| Fee Percentage | Ending Balance | Total Fees Paid |

| 0.05% (Low-Cost Index) | ~$750,000 | ~$11,000 |

| 1.00% (Typical Managed Fund) | ~$570,000 | ~$190,000 |

You are essentially paying a stranger $179,000 to do something a computer can do better. Stick to low-cost providers like Vanguard, Fidelity, or Charles Schwab. For a deeper dive into how fees destroy wealth, check out Vanguard’s breakdown on investment costs.

5. Build a “Career Moat” (Increasing Your Top Line)

“You can only cut your expenses so far before you’re living in a box. However, your income potential is theoretically infinite. That’s why many personal finance tips focus not only on saving money, but also on increasing your earning potential.”

“Expert wealth builders don’t just save; they aggressively increase their ‘top line.’ This means building a career moat—skills that are rare and valuable. Many modern personal finance tips also emphasize skill development and income growth as key parts of long-term wealth building.”

- Negotiation: Most people accept the first salary offer they get. Negotiating just $5,000 more on your starting salary can result in over $500,000 in additional earnings over a 35-year career when compounded.

- Continuous Learning: If your skills are the same today as they were three years ago, you are becoming obsolete.

6. Automate Your “Wealth Gap”

The Wealth Gap’ isn’t just a socioeconomic term; it’s the space between your income and your lifestyle. The wider the gap, the faster you get rich. That’s why practical personal finance tips often encourage living below your means while steadily increasing your income.

The problem is Lifestyle Creep. When you get a raise, your brain immediately starts thinking about a nicer car or a better bottle of wine. To combat this, you must automate the gap. Many personal finance tips recommend automatically directing raises and extra income into savings or investments before lifestyle upgrades take over.

Set your direct deposit so that 50% of every raise goes directly into your brokerage account before it ever touches your checking account. If you never see the money, you won’t miss it. This is the “Pay Yourself First” principle on steroids.

7. Don’t Just Diversify—Rebalance

Everyone knows they should diversify (don’t put all your eggs in one basket). But experts know that diversification is useless without rebalancing.

Let’s say your target is 80% stocks and 20% bonds. After a massive year in the stock market, your portfolio might now be 90% stocks and 10% bonds. You are now over-exposed to a market crash.

Rebalancing is the only time in the financial world where you are forced to sell high and buy low. You sell a bit of the “winners” (stocks) and buy the “underperformers” (bonds) to get back to your target. Doing this once a year is enough to keep your risk in check.

8. Focus on Net Worth, Not Bank Balance

Your bank balance is a snapshot; your Net Worth is the scoreboard. Your net worth is simply:

$$\text{Total Assets} – \text{Total Liabilities} = \text{Net Worth}$$

Assets include your home equity, retirement accounts, and cash. Liabilities are your mortgage, student loans, and credit card debt.

Tracking this monthly allows you to see the big picture. Sometimes your bank account goes down because you moved $10,000 into an investment, but your net worth stayed the same (or grew). This prevents the “panic” that leads to bad financial decisions. Tools like Empower (formerly Personal Capital) are excellent for tracking this automatically.

9. Avoid the “Sunk Cost” Fallacy

This is where psychology meets finance. A sunk cost is money you’ve already spent that you can’t get back.

- “I have to keep this car because I just spent $2,000 on repairs.” (No, the car is still a lemon).

- “I have to hold this stock until it gets back to what I paid for it.” (No, the market doesn’t care what you paid).

Experts make decisions based on the future outlook, not the past cost. If an investment or an asset no longer serves your long-term wealth goals, cut it loose. Your ego is often the most expensive thing you own.

The Best Daily Personal Finance Tips to Secure Your Future

10. Master the “Backdoor Roth” (The High-Earner’s Hack)

If you earn “too much” money, the IRS prevents you from contributing directly to a Roth IRA. However, there is a legal “backdoor” that experts use every year.

- Open a Traditional IRA and contribute after-tax money.

- Immediately convert that Traditional IRA to a Roth IRA.

- Since there are no income limits on conversions, you now have money in a tax-free Roth account.

Note: This can get tricky if you have other Traditional IRA balances due to the “Pro-Rata Rule,” so consult a tax professional or read the Morningstar Guide to Backdoor Roths before pulling the trigger.

Summary: The Wealth-Building Checklist

Wealth isn’t about being “lucky” in the stock market. It’s about being relentlessly consistent with a few high-leverage habits.

- Crush the Big Three: Housing, Transport, Food.

- Invest the Difference: Use the HSA and 401(k) match.

- Check the Fees: Keep your expense ratios under 0.20%.

- Stay the Course: Ignore the headlines and the “next big thing.”

Building wealth is a marathon, but the good news is that the finish line is a lot closer than you think if you stop carrying the extra weight of bad habits and high fees.

What’s one “Big Three” expense you can audit this week to start widening your wealth gap?