Let’s be honest about something right out of the gate: talking about money is usually about as comfortable as a root canal. Most of us never received a formal education on how to manage personal finances. We graduated, landed a job, and were suddenly expected to know how to navigate 401(k) allocations, decipher credit card terms, and magically build wealth.

If you feel completely overwhelmed by your bank accounts, you are definitely not alone. The financial industry loves to make things sound complicated. They use jargon that makes investing and saving sound like an exclusive club you don’t have the password for.

But here is the actual truth: managing your money successfully doesn’t require an MBA. It comes down to a handful of core habits practiced consistently. Whether you are fresh out of college or in your thirties realizing you need to get serious, here are 10 essential personal finance tips for beginners that actually work.

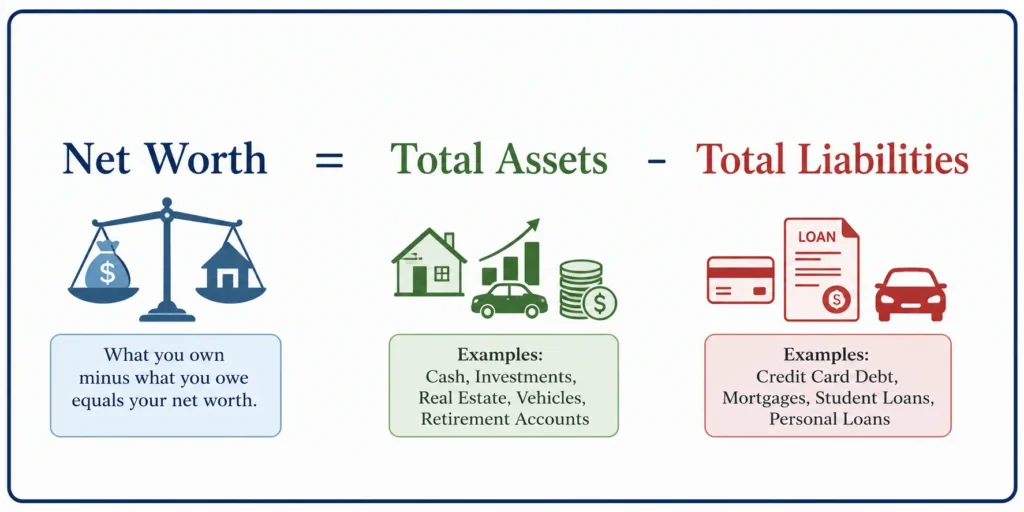

1. Face Your Financial Reality (Calculate Your Net Worth)

Before you can figure out where you’re going, you have to know where you’re standing. It is incredibly common to avoid looking at balances because of the anxiety it causes, but ignorance isn’t bliss—it’s expensive.

Your first step is to calculate your net worth. It’s a simple equation:

Grab a coffee and list everything out.

| Assets (What You Own) | Liabilities (What You Owe) |

| Checking/Savings Balance | Credit Card Balances |

| Retirement Accounts (401k, IRA) | Student Loans |

| Resale value of your car | Auto/Personal Loans |

| Any investment accounts | Mortgage (if applicable) |

If that final number is negative, do not panic. It is completely normal for beginners. The goal isn’t to feel bad; it’s to establish a baseline. What gets measured gets managed.

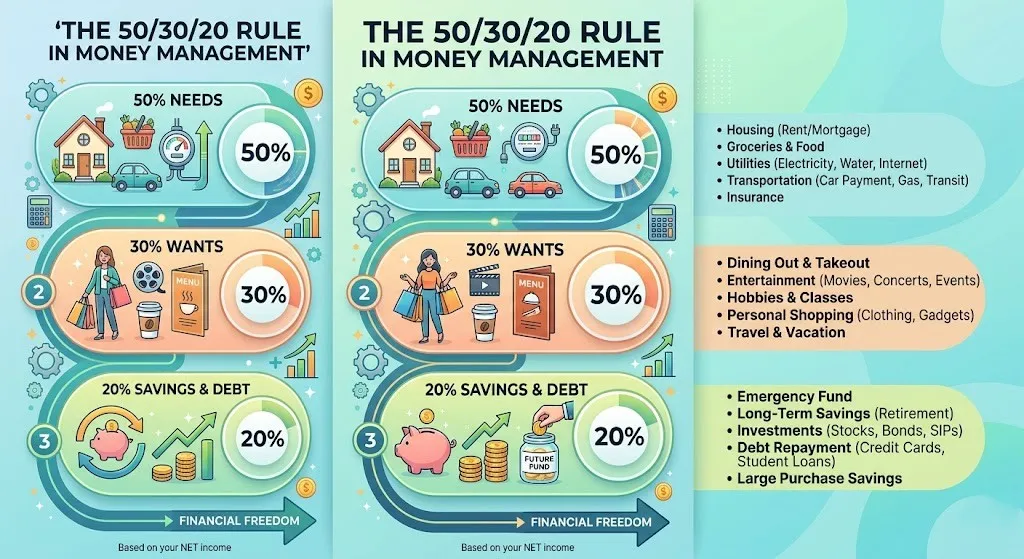

2. Adopt the 50/30/20 Budgeting Framework

The word “budget” often feels like a straitjacket. Instead, think of it as a spending plan. For beginners, the 50/30/20 rule (popularized by Senator Elizabeth Warren) is the perfect starting point because it offers structure without micromanagement.

- 50% for Needs: Rent, groceries, utilities, and minimum debt payments.

- 30% for Wants: Dining out, Netflix, hobbies, and travel.

- 20% for Savings and Investing: Emergency funds and retirement.

Pro Tip: If your “Needs” are taking up 70% of your income, you have a structural issue. Check outNerdWallet’s Budget Calculatorto see how your current spending stacks up.

3. Build a “Sleep At Night” Emergency Fund

Life has a funny way of throwing expensive problems at you right when you least expect it. If you’re relying on a credit card to cover a blown tire, you’re just turning a bad day into a long-term interest-bearing debt.

- Starter Fund: Save $1,000 to $2,000 as fast as you can.

- The Reserve: Once high-interest debt is gone, build this to cover 3–6 months of living expenses.

Keep this money in a High-Yield Savings Account (HYSA). You can compare the best current rates at Bankrate to ensure your emergency fund is actually earning its keep.

4. Declare War on High-Interest Debt

High-interest debt (like credit cards with 20%+ APR) is an absolute wealth killer. It’s a financial emergency. There are two primary ways to attack it:

- The Debt Snowball: Pay the smallest balance first for the psychological “win.”

- The Debt Avalanche: Pay the highest interest rate first to save the most money mathematically.

Pick the one you’ll actually stick to. If you need a tool to help you visualize the finish line, Undebt.it is a fantastic free resource for mapping out your payoff plan.

5. Automate Everything You Can

Human beings are flawed when it comes to discipline. If you have to decide to save every month, you’ll eventually find a reason not to. The secret to building wealth easily is taking your own willpower out of the equation.

- Automate Savings: Have a portion of your paycheck sent directly to your savings/investment account.

- Automate Bills: Set utilities and minimum debt payments to auto-pay to avoid late fees and protect your credit score.

6. Maximize Your Employer Match (Free Money!)

If your company offers a 401(k) match, you need to contribute at least enough to get the full amount. This is a guaranteed 100% return on your money. There is nowhere else in the financial world where you can get a return like that safely.

If you aren’t sure how your 401(k) works, Investopedia’s 401(k) guide breaks down the tax advantages and withdrawal rules in plain English.

Expert Personal Finance Tips to Help You Build Long-Term Wealth

7. Understand and Protect Your Credit Score

Your credit score is essentially your “adult GPA.” It impacts your ability to rent apartments, buy insurance, and get a mortgage.

How your FICO score is calculated:

- Payment History (35%): Pay on time, every time.

- Amounts Owed (30%): Keep your “utilization” low (under 30% of your limit).

- Length of History (15%): Don’t close old accounts.

Important: You are entitled to one free credit report from each bureau every year. Go to AnnualCreditReport.com (the only site authorized by Federal law) to check for errors.

8. Start Investing Yesterday (Keep It Boring)

Money sitting in a checking account loses purchasing power every year due to inflation. To build wealth, your money has to grow. But investing doesn’t mean “day trading” or buying the latest crypto coin.

- Roth IRA: Fund it with after-tax money so it grows tax-free.

- Index Funds/ETFs: Buy a little piece of everything (like the S&P 500).

For a “set it and forget it” philosophy, read up on the Bogleheads approach, which focuses on low-cost, diversified index funds.

9. Beware the Trap of Lifestyle Creep

Lifestyle creep happens when your expenses rise to meet your income. You get a raise, so you get a nicer car. You get a bonus, so you upgrade your apartment. Suddenly, you’re making $20k more but have no more cash than you did before.

The Fix: When you get a raise, allocate 50% of the increase to your lifestyle and 50% to your savings/debt goals. You get to celebrate, but your net worth grows too.

10. Set SMART Financial Goals

“I want to be rich” is a wish, not a goal. To make progress, you need goals that are Specific, Measurable, Achievable, Relevant, and Time-bound.

- Bad Goal: “I want to save for a house.”

- SMART Goal: “I will save $20,000 for a down payment in 24 months by automating $833 a month into my HYSA.”

When your goals are crystal clear, it’s much easier to say “no” to impulse buys.

The Bottom Line

Personal finance is 20% head knowledge and 80% behavior. You don’t need to be a math genius; you just need to be consistent. Start small—calculate your net worth this weekend or set up one automated transfer. Take it one step at a time, and your “future self” will thank you.